Book a demo or watch 3-minute tour

Learn to recognise the warning signs that your accounting system is holding you back - from endless month-ends and manual workarounds to risky on-premises servers - and discover how to calculate the true cost of doing nothing.

Learn to recognise the warning signs that your accounting system is holding you back - from endless month-ends and manual workarounds to risky on-premises servers - and discover how to calculate the true cost of doing nothing.

When you're considering a change to your finance system, the stakes feel high. If you get it wrong, you might fear the fallout could overshadow years of achievements – and that you’ll be remembered for eons as 'That Genius Who Chose This Damn Finance System'.

"A lot of FDs still bear the scars from changing systems in the past,” says Richard Woolgar, who has helped a lot of organisations change their software in his role as Head of Outsourcing for leading professional services firm Armstrong Watson.

“Just mention the topic and you’ll likely detect a little roll of the eyes or hear a deep sigh as they recall a nightmare project from the past.

“The pain factor is the biggest barrier to changing systems, even when people know they really need to.”

Louise Zandstra, Finance Director at the National Youth Theatre, has been through several system changes in past jobs. “It is a big thing – and although it mainly affects the finance department, it has an impact on everybody else,” she says.

“I've been involved in implementations that went horribly wrong. For example, I worked for a large charity that decided to implement at year-end, which was a tricky time, and months later, they still couldn't get opening balance reports out of the finance system.”

Could you actually be fired for getting a change of systems wrong? “It’s more that you might end up wanting to quit,” says Lauren McCluskey, Head of Virtual Finance Function at accountancy and business advisory firm AAB.

Lauren has gone through system changes as an accountant in practice and as an FD in industry. “If you're the leader of the finance team and the change hasn't gone well, it is soul-destroying. It will take over your life,” she says.

So it’s not surprising that many finance leaders opt to persevere with the systems they have – even when those systems are holding them back and stifling growth.

Fortunately, there is a right way to change. What follows is a guide to switching finance systems without the soul-destroying part.

We’ve drawn on insights from FDs, accountants, software experts and change consultants. They told us:

✅ Why you may already know it's time for a change

✅ 7 key questions to ask at the outset

✅ Lots more questions in a handy checklist

✅ How to count the cost of doing nothing

(And while we’ve tried to keep this guide light and accessible, we know you won’t be casting aside The Thursday Murder Club and declaring you’ve found your next beach read.)

Perhaps the grumbles from finance users have grown too loud to ignore. Maybe a frustrated CEO has turned the issue into your number one concern. Or possibly you’re new to the organisation and the flaws in the system were glaringly obvious from day one.

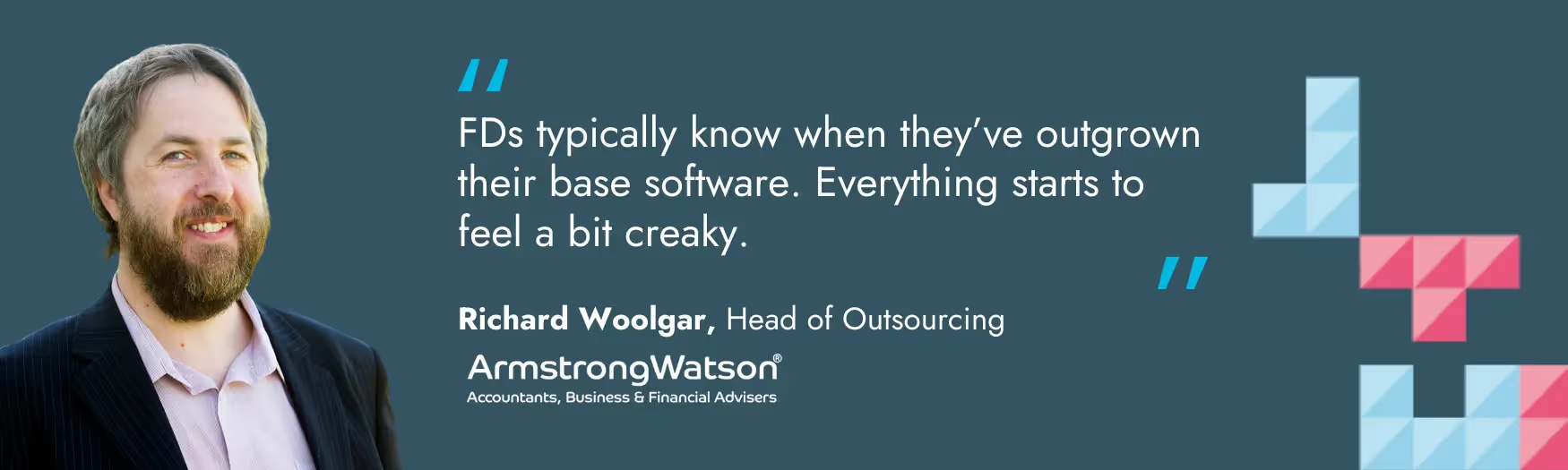

“I think FDs typically know when they’ve outgrown their base software. Everything starts to feel a bit creaky at the edges,” says Richard Woolgar, Head of Outsourcing at Armstrong Watson.

Lauren McCluskey, Head of Virtual Finance Function at AAB, says: “There’ll usually be increasing frustration within the finance team and within the business that the system is just not doing what you need it to do.”

Often, an incoming FD will instigate the move. Louise Zandstra, Head of Finance at the National Youth Theatre, says: “Sometimes, you come into an organisation, take a look and think: ‘Oh my goodness – Why?’

“If people have been working somewhere for a long time, they get used to the way things work, so it takes a newcomer to bring a fresh pair of eyes to the situation and say: Why are we doing this? Why are we carrying out these long-winded processes with six spreadsheets when there are better ways to do things?

“In the charity world, particularly in smaller charities, you might have to limp along with whatever system you’ve got for longer than you want. But eventually something happens – perhaps the licence fees go up again or yet another manual process has to be introduced – and that event becomes the last straw.”

But upgrading your finance software only makes sense if the process of change would be less painful than sticking with the system you’ve got. And it’s fair to say most people put off the change until using the old system really hurts. A lot.

Does all the management information you need come rolling out of the finance system at month-end with minimal effort on your part? Or do you have to toil for days in Excel spreadsheets to produce the figures that other people think just appear by magic?

Reporting is probably the key test of your system’s efficiency.

“Are you getting what you want out of the system every month – and how easy is that process?” asks Richard Woolgar, Head of Outsourcing at Armstrong Watson.

“For example, when someone asks an FD ‘How much did this project make for us?’, the FD needs to be able to refer to a standard report that comes out of the system monthly.”

Lauren McCluskey says: “If your system isn't providing you the reporting and the information that you need on a day-to-day basis, without a lot of manual intervention or workarounds, it's normally time to look at something else.”

Frances Kay, a Partner with business advisers and accountants TC Group as well as Director of the independent app resource App Advisory Plus, says: “The people who come to me are usually moving away from desktop software to a cloud product – and their problem is usually about the output of data.

“The CFO will be asking for information that they can’t get out of the product at all or they’re chasing figures from months ago.

“If a CFO doesn’t have the numbers, it’s hard to form a serious strategy and do everything else they have to do. And these days it’s not just about the balance sheet and P&L. There are a lot more analytics that people want, a lot of which affects operations.”

For decision makers, access to real time data is essential, says Jamie Allen, Founder and CEO of the technology advisory firm 4PointZero. “Businesses need to know whether they’re pricing correctly or where they might be overspending. In hospitality, for instance, fluctuations in food procurement costs or staffing expenses might require immediate menu price adjustments,” he says.

“In a professional services firm, rising costs may mean increasing charge out rates to maintain profitability. The key is acting on this information now, rather than realising six months down the line that margins have been squeezed.

“Historically, finance and operations worked in silos, often relying on separate data sets. Many businesses still operate this way, with operations presenting an optimistic outlook while finance delivers a starkly different reality. But with modern software, these teams should be working with a single, reconciled source of truth.”

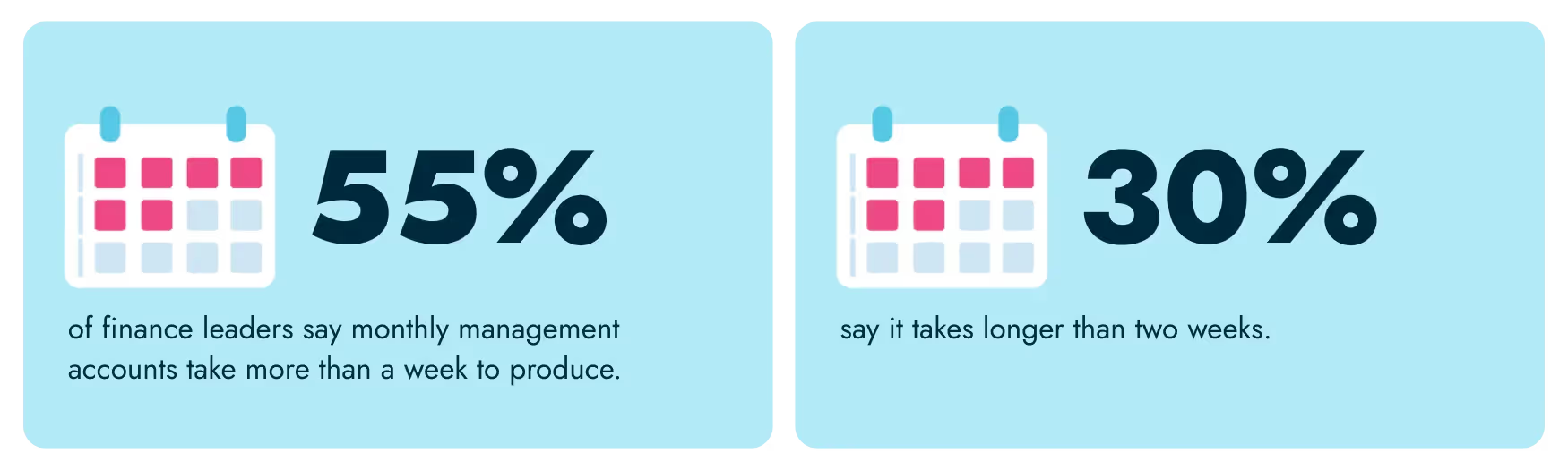

Does your month-end tend to go on all month?

Putting together the monthly management accounts takes longer than a week for 55% of finance leaders, research by iplicit has found. Nearly a third of those leaders report that it takes longer than two weeks.

For most organisations, that just isn’t fast enough.

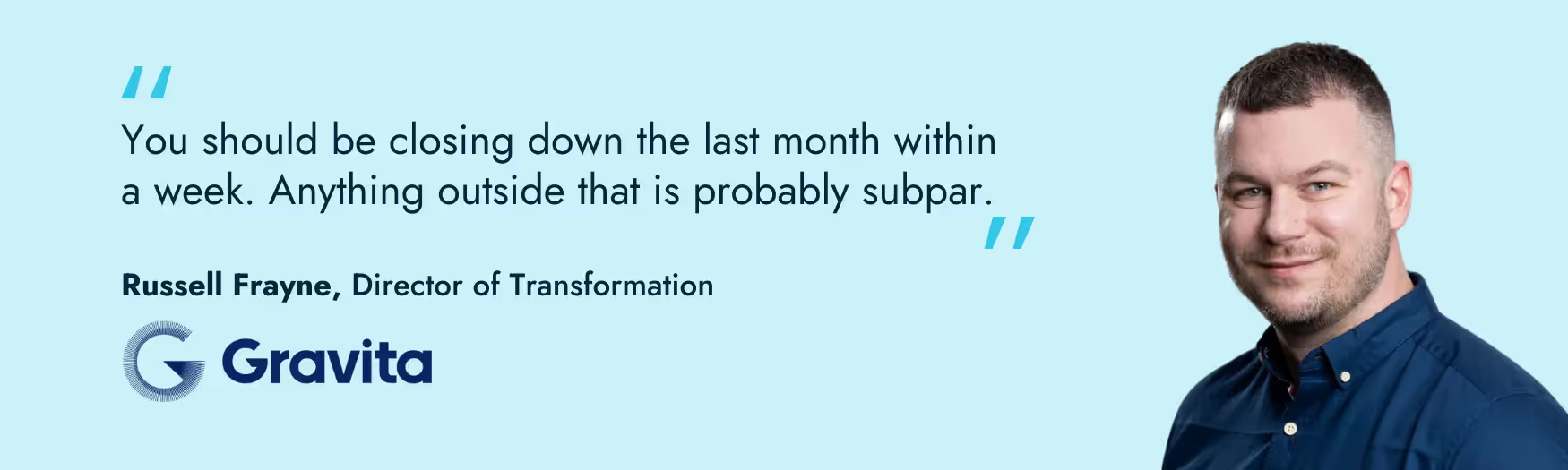

“You should be closing within a week. Anything outside of that is probably subpar,” says Russell Frayne, who implements a wide range of systems as Director of Transformation at tech-enabled accountants Gravita.

“A longer closedown means whatever data you’re looking at is already out of date.”

Lauren McCluskey says: “The length of your month-end is normally a key question. Are you getting the board reporting and financial reporting out in the way you need to? Is the business able to use the system easily? And are people able to get the budget, the forecasts and the project spend out of the system nicely?”

What do your people do all day? Taking a thorough look at your processes – and how much staff time they take up – will help reveal any duplication and inefficiency.

Are people bogged down in data entry? Do they have to rekey information from one place to another because different systems don’t talk to each other? Do purchase invoices take lengthy tours around different parts of the organisation before they’re approved?

“If you’ve got the same information passing through multiple touch points – involving different people, systems and processes – that’s absolutely an indicator that things are not as efficient as they should be,” says Russell Frayne.

Often, workarounds will have evolved because the software couldn’t keep pace with growth.

“The limitations that both businesses and charities can run up against are either about transaction volumes or complexity,” says Richard Woolgar.

“Often, the capabilities of the system have been stretched to the limit and people have built unwieldy processes, with workarounds upon workarounds and a lot of work happening in spreadsheets outside the finance system.”

Lauren McCluskey adds: “You often see duplication and inefficiency crop up when different departments own different bits of the system and nobody has overall responsibility. The more these different teams make bespoke additions to the system, the more unwieldy it becomes.”

Louise Zandstra says: “Often, you have spreadsheets at both ends of a process – some for information that needs to go into the system and some for information that’s coming out. So the system isn’t doing any of the work for you; it’s just a repository for data and all the work goes on outside the system, requiring you to capture data two or even three times. You should be capturing the data just once and then the system should be using it to provide the management information you really need.”

It isn’t just the finance team that will feel the strain. “Inefficiency affects operational teams as well,” says Frances Kay.

“When you’ve got someone filling in staff expenses on a spreadsheet, everyone’s going to moan about that kind of thing until eventually a conversation starts about how to do things better.

Are you using a basic finance system connected to a lot of third-party applications? Those plugged-in apps might be good at doing things that the accounting software can’t. But as the number of applications rises, so does the cost and the risk that a connection between two parts of the tech stack could fail.

“There comes a tipping point where you create a Frankenstein system, where so many things are bolted together that you’ve created a monster,” says Russell Frayne.

“You can end up with a lot of different apps to log into. How many different single sign-on (SSO) procedures or multi-factor authentication (MFA) processes do you have to use just to access your finance system?

“It might all be fine but if you’re controlling this for a whole business and you have to manage 10, 15, 20 apps – and be accountable for the price – that can be quite overwhelming.

“You should also look at the nature of those connected apps. Are they off-the-shelf tools for tasks such as data capture, reporting or stock management? A more powerful finance system could handle tasks like that. But if there’s something that’s more bespoke or unique to your business or sector, you might feel that particular piece of software is non-negotiable and would have to be integrated with any new system.”

We’re all familiar with the hackneyed portrayal of finance people as uber-cautious, buttoned-down bean counters. But sometimes finance teams are taking more risks than they might realise.

Are you happy that people have access to the information they need in your finance system without seeing anything they shouldn’t?

Are you confident that the right permissions are in place to prevent fraud and error?

How’s your cybersecurity? Are fixes and updates applied automatically to your software or do you stop everything and install patches?

Is your data stored in the cloud – and if not, what would you do if the server on your premises was hit by theft, damage or breakdown? Could the team carry on working if nobody could get into the office?

“Just getting into the cloud is a basic requirement and is sort of happening naturally without us as advisers having to push it,” says Frances Kay.

“In terms of infrastructure, security and integration with other products, almost everybody should be moving to a cloud product.”

At the Blackpool Grand Theatre, finance was the last department using an on-premises server with no back-up. That made people very conscious of the need to change systems.

“Virtually everything had been moved into the cloud and it was just finance on this end-of-life server,” says Mark Preston, Head of Business and Finance. “If we’d had a fire or a flood, we would have lost all our finance records.”

Finance can be quite the white-knuckle ride when you think about it.

"There are really only two reasons to change systems," says Jamie Allen, Founder of 4PointZero. "Either you are solving a problem or you are pursuing an ambition."

"When I sit down with a potential client, I ask, ‘Where are you going? And do your current processes support that growth?’ That is the ambition part," he explains.

If your systems are already under strain and your organisation is aiming to grow, things are unlikely to get easier.

"We often meet businesses that have scaled to a point where it no longer makes sense to keep hiring more people. That is simply not efficient," Jamie says.

"Humans care whether they are processing one transaction or a million. Computers do not. Many businesses reach a stage where that difference really starts to matter, and increasing headcount is no longer a sustainable solution."

Can you grow by your likely rate without swelling the finance payroll by the same amount? If not, you’ll need to change things.

We’ve seen the dangers of overstraining a basic finance system. But is it possible that you’re not working that system hard enough? It’s a question to think about before you make a change.

Have you exhausted your current software’s ability to improve processes? Have you kept on top of product updates and release notes? Does the vendor offer webinars to ensure you’re getting best value from the system?

“A lot of people think their software can’t do something because it couldn’t do it when they first set it up,” says Lauren McCluskey. “But that might have changed. It’s important to ensure you’re getting the best use of the product you’ve got before looking for something new.”

Russell Frayne adds: “Sometimes, people are just not using their current system well.

“When we’re fact finding with a client, our first questions are always: Is the current system the right one for that client? Is it possible they’re just not using it properly?

“Clients love it when we tell them they don’t have to spend a lot of money and that all they need is for us to show them how to use the system better – and perhaps pay a bit more for more licences.”

Some questions to ask about your current software:

☐ Are you happy with the performance of your system?

☐ Are you happy with the productivity you’re seeing from the system?

☐ Are you happy with staff retention in your finance team? Are you confident that the software isn’t causing staff turnover?

☐ Are you happy your software will scale reliably with your organisation, without a corresponding rise in the number of staff?

☐ Are you confident about the security of the system?

☐ Is your software still being developed?

☐ Are you confident it will be supported if relevant legislation changes?

☐ Does your system ensure data is only available to the correct audience?

☐ Are you confident that processes and controls are sufficient to catch errors and fraud?

☐ Are your systems covered by disaster recovery and business continuity plans?

☐ Is your system providing real time financial information?

☐ Are you happy with the quality of your reporting? Can you analyse data as flexibly as you need to?

☐ Does your MI provide actual vs budget figures and forecasts?

☐ Can you produce management information within 5-10 days of month-end?

☐ Can other people in the organisation serve themselves to the financial data they’re authorised to see?

☐ Does your software use AI to read invoices and match them with supplier records and POs? Does it use machine learning to make these matches better?

☐ Does your system simplify bank reconciliation by matching a bank feed with what’s in your finance system?

☐ Is credit control handled automatically, with appropriate reminders sent from the finance system?

☐ Can budget holders see and approve purchase orders in the system? Can expenses be submitted and authorised electronically?

☐ Do you have electronic workflows and automated processes?

☐ Have you stopped crosschecking all data to see if it’s accurate?

☐ Can your system schedule recurring tasks and processes?

☐ Is your purchase order system effective?

☐ Do you have an electronic audit trail of transaction authorisations?

☐ Does your system provide real-time information?

☐ Can your system handle the transaction volumes you see now and those you expect in the future?

☐ Does the finance system connect smoothly with other software without rekeying of data? ☐ Are you happy with the number of third-party applications connected to the finance system?

☐ Can you see how projects have performed without a lot of work in spreadsheets?

☐ Can you consolidate easily between group entities without manual offline work?

☐ Are you happy that your software is giving value for money? Remember to factor in all licences, third-party plug-ins and any costs from keeping a server.

Answered mostly “yes”? It may be a case of “Don’t change, you’re perfect”.

Answered “no” a few times? Read on. 👇

Are your answers so far indicating it’s time to change? You could now be as excited by thoughts of accounting software as it’s possible for a sensible human being to be. Yet once you look at the cost of a new product, you might be tempted to call the whole thing off.

It’s likely – though not inevitable – that more flexible and powerful software will cost more than your core system at the moment. You may dread trying to justify that price rise to your CEO or board.

“The software cost is normally the biggest number on the page when you start out,” says Russell Frayne.

“But that’s before you consider the savings. The monthly cost for most platforms is fairly insignificant compared with what that platform will do for you, if you implement it properly.”

He has seen system changes that allow clients to redeploy people from the finance team and bring forward revenue-generating ventures by years.

“When people see how a system will remove other costs and perhaps allow them to start a new revenue stream without additional staff, they can see the ROI,” he says.

“But the really scary number is the cost of doing nothing. That cost will keep growing and it can be astronomical.”

Richard Woolgar adds: “There are two kinds of costs from doing nothing. There are the costs of all those inefficient processes but there’s also the cost of not having the right controls in place. That brings the risk of fraud and error and also the risk that, for example, without a good purchase order system, people are buying goods and services for way over the odds.”

To begin counting the cost of doing nothing, you can look again at all that time being taken up by manual and repetitive work – and try multiplying those hours by the cost of employing those staff.

Then you can add any costs for multiple instances of the same software, along with the subscriptions for any third-party apps plugged into the finance system. If you’re hosting a server on your premises, the cost of that needs to be factored in too.

At this point, the case for an upgrade might look undeniable.

Now comes the hard part. Convincing other people.

You probably have a hunch already if you need to change systems. In the words of Darth Vader: “Search your feelings – you know it to be true.”

Try asking these key questions:

Then count the cost of doing nothing - time spent on inefficient processes, server maintenance, multiple software licences, the cost of not having the right controls.

Is the case starting to look compelling?

Book your demo and discover how iplicit can simplify your finance operations, automate manual processes, and give you real-time visibility - wherever you work.